Professional ethics is vital for all professions. It refers to the accepted standards of behavior and values that professionals must follow. Professional organizations establish codes of ethics to guide their members in performing their job functions ethically and maintain their profession’s reputation.

Let’s understand how auditors use professional ethics in the auditing process.

What is Professional Ethics?

Professional ethics refers to the professionally accepted standards of personal and business behavior, values, and guiding principles. It encompasses the personal, organizational, and corporate standards of behavior expected of professionals.

Professionals and those working in acknowledged professions exercise specialist knowledge and skill.

How this knowledge should be governed when providing a service to the public can be considered a moral issue and is termed professional ethics.

Professionals can make judgments, apply their skills, and reach informed decisions in situations that the general public cannot because they have not received the relevant training.

Professional ethics is part of human ethics.

Professional organizations often establish codes of professional ethics to help guide members in performing their job functions according to sound and consistent ethical principles.

Objectives of Professional Ethics

Professional accountants play an important role in building up the economic wellbeing of their community and country with their attitude, behavior, and unique services.

They have common objectives, whether they work in the capacities of external auditors, internal auditors, financial experts, tax experts, and management accountants.

Their common objectives are to perform their duties and responsibilities and attain the highest levels of performance by the ethical requirements to meet the public interest and maintain the accounting profession’s reputation.

Personal self-interest must not prevail over these duties. The IFAC and ICAEW Codes of Ethics help accountants meet these obligations by setting out ethical guidance to be followed.

To achieve these objectives, they must establish creditability, professionalism, quality of service, and confidence.

Acting in the public interest involves having regard for the legitimate interests of clients, government, financial institutions, employees, investors, the business and financial community, and others who rely upon the objectivity and integrity of the accounting profession to support the dignity and orderly functioning of commerce.

In summary, accountants need to have an ethical code because people rely on them and their expertise. It is important to note that this reliance extends beyond clients to the general community.

Accountants deal with a range of issues on behalf of clients. They often have access to confidential and sensitive information.

Auditors claim to give an independent view. It is, therefore, critical that accountants are independent.

Compliance with a shared set of ethical guidelines also protects accountants, as they cannot be accused of behaving differently from other accountants.

Codes of Professional Ethics

Here we will describe the two well-known codes of professional ethics;

- IFAC code of ethics for professional accountants,

- AICPA code of professional conduct.

IFAC Code of Ethics for Professional Accountants

A distinguishing mark of the accountancy profession is its acceptance of the responsibility to act in the public interest.

In acting in the public interest, a professional accountant should observe and comply with the ethical requirements of this Code.

A professional accountant is required to comply with the following five fundamental principles:

1. Integrity

A professional accountant should be straightforward and honest in all professional and business relationships.

2. Objectivity

A professional accountant should not allow bias, conflict of interest, or undue influence of others to override professional or business judgments.

3. Professional Competence and Due Care

A professional accountant must maintain professional knowledge and skill at the level required to ensure that a client or employer receives competent professional service based on current developments in practice, legislation, and techniques.

Professional accountants should act diligently and by applicable technical and professional standards when providing professional services.

4. Confidentiality

A professional accountant should respect the confidentiality of information acquired from professional and business relationships and should not disclose any such information to third parties without proper and specific authority unless there is a legal or professional right or duty to disclose it.

Confidential information acquired from professional and business relationships should not be used for the professional accountant’s or third parties’ advantage.

5. Professional Behavior

A professional accountant should comply with relevant laws and regulations and avoid any action that discredits the profession.

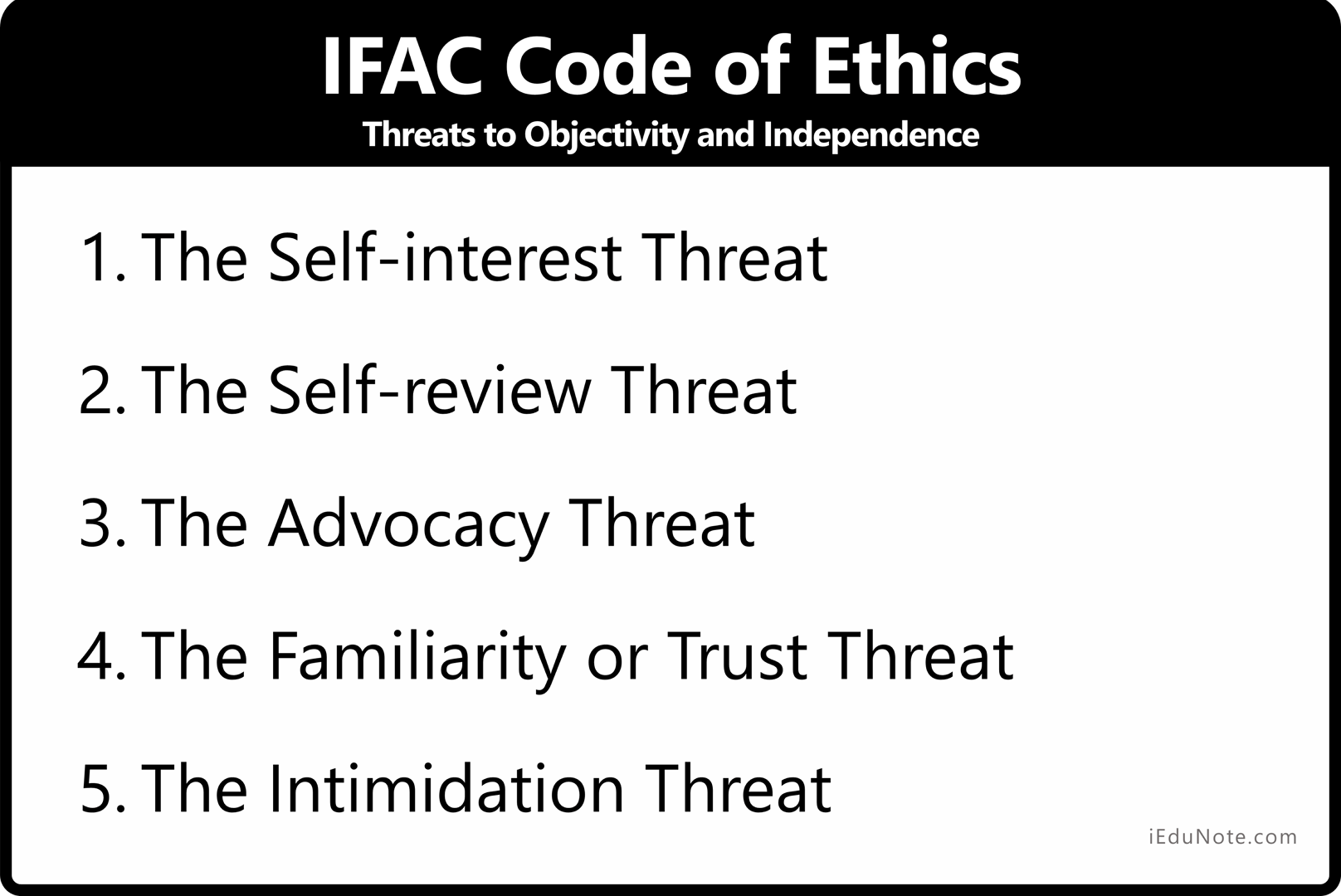

IFAC Code of Ethics – Threats to Objectivity and Independence

The IFAC Code of Ethics works on the basis that an assurance firm’s integrity, objectivity, and independence are subject to various threats and that the firm must have safeguards to counter these threats.

6 threats to audit objectivity and independence are;

1. The Self-interest Threat

Self-interest threat occurs when a firm, network firm, or an assurance team member could benefit from a financial interest in or other self-interest conflicts with an assurance client.

2. The Self-review Threat

Self-review threat occurs when

- any product or judgment of a previous assurance engagement or non-assurance engagement needs to be re-evaluated in reaching conclusions on the assurance engagement; or

- a member of the assurance team was previously a director or officer of the assurance client or was an employee in a position to exert direct and significant influence over the subject matter of the assurance engagement.

3. The Advocacy Threat

Advocacy threat occurs when a firm, a member of the assurance team, or a member of the network firm, as applicable, promotes or may be perceived to promote an assurance client’s position or opinion to the point that objectivity may or may be perceived to be, compromised.

Such might be the case if a firm or an assurance team member were to subordinate their judgment to that of the client.

4. The Familiarity or Trust Threat

Familiarity threat occurs when a close relationship with an assurance client, its directors, officers, or employees, a firm, or a member of the assurance team or network firm, as applicable, becomes too sympathetic to the client’s interests.

5. The Intimidation Threat

Intimidation threat occurs when a member of the assurance team may be deterred from acting objectively and exercising professional skepticism by threats, whether actual or perceived, from the directors, officers, or employees of an assurance client.

6. Safeguards

- The auditor’s responsibility is to ensure that they remain independent of the client entity.

- When no effective safeguards are available to reduce the threats to an acceptable level, the only possible actions are to eliminate the activities or interest creating the threat or to refuse to accept or continue the assurance engagement.

- In assessing threats to independence and the possible safeguards to mitigate or eliminate these threats, auditors are required at all times to consider what is in the public interest.

- It is also important to note that adopting certain safeguards may not address “independence in appearance.”

ICAEW Code – The five fundamental principles of the ICAEW Code

ICAEW’s Code of Ethics (the Code) applies to all members, students, affiliates, employees of member firms, and, where applicable, member firms in all of their professional and business activities, whether remunerated or voluntary.

This is influenced by the guidance of IF AC (the International Federation of Accountants, of which ICAEW is a member).

The ICAEW Code states that professional accountants are expected to follow the guidance contained in the fundamental principles in all of their professional and business activities, whether carried out with or without reward and in other circumstances where to fail to do so would bring discredit to the profession.

The code has been derived from the International Ethics Standards Board of Accountants (IESBA) Code of Ethics issued in July 2009 by the International Federation of Accountants. Accordingly, compliance with the remainder of this Code will ensure compliance with the principles of the IESBA Code.

Paragraph numbering in the rest of this Code replicates that used in the IESBA Code of Ethics, except in respect of Sections 221,241 and Part D, which have no direct equivalent in the IESBA Code of Ethics.

ICAEW’s code of ethics in place to 31 December 2010 replaced ICAEW’s guide to professional ethics on 1 September 2006. A revised code of ethics applies from 1 January 2011.

The substance of this code is the same as our previous Guide to Professional Ethics, but the layout and structure of the new code are more users friendly.

The ICAEW Code implements the IFAC Code above so that following it ensures compliance with the IFAC Code. The five fundamental principles of the ICAEW Code

The second section of the AICPA’s code of professional conduct consists of 11 enforceable rules as listed below:

1. Integrity

A professional accountant should be straightforward and honest in all professional and business relationships.

2. Objectivity

A professional accountant should not allow bias, conflict of interest, or undue influence of others to override professional or business judgments.

3. Professional Competence and Due Care

A professional accountant has a continuing duty to maintain professional knowledge and skill at the level required to ensure that a client or employer receives competent professional services based on current developments in practice, legislation, and techniques.

Professional accountants should act diligently and by applicable technical and professional standards.

4. Confidentiality

A professional accountant should respect the confidentiality of information acquired as a result of professional and business relationships and should not disclose any such information to third parties without proper and specific authority unless there is a legal or professional right or duty to disclose it.

Confidential information acquired as a result of professional and business relationships should not be used for the personal advantage of the professional accountant or third parties.

5. Professional Behavior

A professional accountant should comply with relevant laws and regulations and should avoid any action that discredits the profession.

APB Ethical Standards

U.K. auditors are also subject to APB’s Ethical Standards. The APB is the Auditing Practices Board in the U.K., which also issues auditing standards (adopted from IFAC, which creates them).

APB has issued ethical standards with which U.K. auditors must comply when carrying out U.K. audits. They are as follows:

- E.S. 1: Integrity, objectivity, and independence

- E.S. 2: Financial, business, employment, and personal relationships

- E.S. 3: Long association with the audit engagement

- E.S. 4: Fees, remuneration, and evaluation policies, litigation, gifts, and hospitality

- E.S. 5: Non-audit services provided to audit clients

There is also an E.S. with provisions available for smaller entities, which is not examinable. This offers exemptions and special rules to the auditors of smaller entities.

These standards were developed about the IFAC Code of Ethics and the E.C. Recommendation on the independence of statutory audits.

AICPA Code of Professional Conduct

The Code of Professional Conduct of the American Institute of Certified Public Accountants consists of two sections;

The Principles provide the framework for the Rules which govern the performance of professional services by members. The Council of the American Institute of Certified Public Accountants is authorized to designate bodies to promulgate technical standards under the Rules, and the bylaws require adherence to those rules and standards.

A few definitions taken from the AICPA Code of Professional Conduct must be understood to minimize misinterpretation of the rules.

Client. Any person or entity other than the member’s employer engages a member or member’s firm to perform professional services or a person or entity concerning which professional services are performed.

Firm. A form of the organization permitted by law or regulation whose characteristics conform to resolutions of the council of the AICPA and that is engaged in public practice.

Institute. The American Institute of Certified Public Accountants.

Member. A member, associate member, or international associate of the American Institute of Certified Public Accountants.

Public practice. Public practice consists of the performance of professional services for a client by a member or a member’s firm.

A. The Principles – AICPA Code of Professional Conduct

The principles of the Code of Professional Conduct of the American Institute of Certified Public Accountants express the profession’s recognition of its responsibilities to the public, clients, and colleagues.

The second section of the AICPA’s code of professional conduct consists of 11 enforceable rules as listed below:

1. Responsibilities: ET Section 52 – Article I

In carrying out their professional responsibilities, members should exercise sensitive professional and moral judgments in all their activities.

2. The Public Interest: Section ET 53 – Article II

Members should accept the obligation to act in a way that will serve the public interest, honor the public trust, and demonstrate a commitment to professionalism.

3. Integrity: Section ET 54 – Article III

Members should perform all professional responsibilities with the highest sense of integrity to maintain and broaden public confidence.

4. Objectivity and Independence: Section ET 55 – Article IV

A member should maintain objectivity and be free of conflicts of interest in discharging professional responsibilities. A member in public practice should be independent in fact and appearance when providing auditing and other attestation services.

5. Due Care:Section ET 56 – Article V

A member should observe the profession’s technical and ethical standards, strive continually to improve competence and service quality and discharge professional responsibility to the best of the member’s ability.

A member of public practice should observe the Principles of the Code of Professional Conduct in determining the scope and nature of services provided.

B. The Rules – Rules of Conduct According to the AICPA Code of Professional Conduct

The second section of the AICPA’s code of professional conduct consists of 11 enforceable rules as listed below:

Rule 101 – Independent

A member in public practice shall be independent in the performance of professional services as required by standards promulgated by bodies designated by the council.

In performing an attest engagement, a member should consult the rules of;

- their state board of accountancy,

- his or her state CPA society,

- the Public Company Accounting Oversight Board, and the U.S. Securities and Exchange Commission (SEC) if the member’s report will be filed with the SEC,

- the U.S. Department of Labor (DOL), if the member’s report will be filed with the DOL,

- the Government Accountability Office (GAO) if a law, regulation, agreement, policy, or contract requires the member’s report to be filed under GAO regulations, and

- any organization that issues or enforces standards of independence would apply to the member’s engagement.

Such organizations may have independence requirements or rulings that differ from (e.g., maybe more restrictive than) the AICPA.

Independence shall be considered to be impaired if:

- During the period of the professional engagement, a covered member.

- Had or was committed to acquiring any direct or material indirect financial interest in the client.

- Was a trustee of any trust or executor, or administrator of any estate if such trust or estate had or was committed to acquiring any direct or material indirect financial interest in the client and

- The covered member (individually or with others) had the authority to make investment decisions for the trust or estate; or

- The trust or estate owned or was committed to acquiring more than 10 percent of the client’s outstanding equity securities or other ownership interests; or

- The value of the trust’s or estate’s holdings in the client exceeded 10 percent of the total assets of the trust or estate.

- Had a joint closely-held investment that was material to the covered member.

- Except as specifically permitted in interpretation 101-5, had any loan to or from the client, any officer or director of the client, or any individual owning 10 percent or more of the client’s outstanding equity securities or other ownership interests.

- During the professional engagement period, a partner or professional employee of the firm, his or her immediate family, or any group of such persons acting together owned more than 5 percent of a client’s outstanding equity securities or other ownership interests.

- During the period covered by the financial statements during the period of the professional engagement, a firm, partner or professional employee of the firm was simultaneously associated with the client as a(n)

- Director, officer, or employee, jor in any capacity equivalent to that of a member of management;

- The promoter, underwriter, voting, trustee; or

- Trustee for any pension or profit-sharing trust of the client.

Rule 102 – Integrity and Objectivity

In the performance of any professional service, a member shall maintain objectivity and integrity, shall be free of conflicts of interest, and shall not knowingly misrepresent facts or subordinate his or her judgment to others.

A member shall be considered to have knowingly misrepresented facts in violation of rule 102 when he or she knowingly;

- Makes, permits, or directs another to make materially false and misleading entries in an entity’s financial statements or records; or

- Fails to correct an entity’s financial statements or records that are materially false and misleading when they have the authority to record an entry; or

- Signs, permits, or directs another to sign a document containing materially false and misleading information.

Rule 201 – General Standards

A member shall comply with the following standards and any interpretations thereof by bodies designated by the council.

- Professional Competence. Undertake only those professional services that the member or the member’s firm reasonably expects to be completed with professional competence.

- Due Professional Care. Exercise due professional care in the performance of professional services.

- Planning and Supervision. Adequately plan and supervise the performance of professional services.

- Sufficient Relevant Data. Obtain sufficient relevant data to afford a reasonable basis for conclusions or recommendations about any professional services performed.

A member’s agreement to perform professional services implies that the member has the necessary competence to complete those professional services according to professional standards, applying his or her knowledge and skill with reasonable care and diligence. Still, the member does not assume responsibility for the infallibility of knowledge or judgment.

Competence to perform professional services involves both the technical qualifications of the member and the member’s staff and the ability to supervise and evaluate the quality of the work performed.

Competence relates both to a knowledge of the profession’s standards, techniques, and the technical subject matter involved and to the capability to exercise sound judgment in applying such knowledge in the performance of professional services.

The member may have the knowledge required to complete the services by professional standards before a performance.

In some cases, however, additional research or consultation with others may be necessary during the performance of the professional services.

This does not ordinarily represent a lack of competence but is a normal part of the performance of professional services.

However, suppose a member cannot gain sufficient competence through these means. In that case, the member should suggest, in fairness to the client and the public, the engagement of someone competent to perform the needed professional service independently or as an associate.

Rule 202 – Compliance with Standards

A member who performs auditing, review, compilation, management consulting, tax, or other professional services shall comply with standards promulgated by bodies designated by the council.

Rule 203 – Accounting Principles

A member shall not;

(1) Express an opinion or state affirmatively that the financial statements or other financial data of any entity are presented in conformity with GAAP (generally accepted accounting principles), or

(2) state that he or she is not aware of any material modifications that should be made to such statements or data for them to conform with generally accepted accounting principles if such statements or data contain any departure from an accounting principle promulgated by bodies designated by the council to establish such principles that have a material effect on the statements or data taken as a whole.

If, however, the statements or data contain such a departure and the member can demonstrate that due to unusual circumstances, the financial statements or data would otherwise have been misleading, the member can comply with the rule by describing the departure, its approximate effects, if practicable, and the reasons why compliance with the principle would result in a misleading statement.

Rule 301 – Confidential Client Information

A member in public practice shall not disclose any confidential client information / without the specific consent of the client.

This rule shall not be construed;

- to relieve a member of his or her professional obligations under rules 202 and 203,

- to affect in any way the member’s obligation to comply with a validly issued and enforceable subpoena or summons, or to prohibit a member’s compliance with applicable laws and government regulations,

- to prohibit review of a member’s professional practice under AICPA or state CPA society or Board of Accountancy authorization, or

- to preclude a member from initiating a complaint with, or responding to any inquiry made by, the professional ethics division or trial board of the Institute or a duly constituted investigative or disciplinary body of a state CPA society or Board of Accountancy.

Members of any of the bodies; identified in (4) above and members involved with professional practice reviews identified in (3) above shall not use to their advantage or disclose any member’s confidential client information that comes to their attention in carrying out those activities.

This prohibition shall not restrict members’ exchange of information in connection with the investigative or disciplinary proceedings described in (4) above or the professional practice reviews described in (3) above.

Rule 301 prohibits a public practice member from disclosing confidential client information without the client’s specific consent. The rule provides that it shall not be construed to prohibit the review of a member’s professional practice under AICPA or state CPA society authorization.

For rule 301, a review of a member’s professional practice is hereby authorized to include a review in conjunction with a prospective purchase, sale, or merger of all or part of a member’s practice.

The member must take appropriate precautions (for example, through a written confidentiality agreement) so that the prospective purchaser does not disclose any information obtained in the course of the review since such information is deemed to be confidential client information.

Members reviewing practice in connection with a prospective purchaser or merger shall not use to their advantage nor disclose any member’s confidential client information that comes to their attention.

Rule 302 – Contingent fees

A member in public practice shall not:

- Perform for a contingent fee any professional services for, or receive such a fee from a client for whom the member or the member’s firm performs,

- an audit or review of a financial statement; or

- a compilation of a financial statement when the member expects, or reasonably might expect, that a third party will use the financial statement and the member’s compilation report does not disclose a lack of independence; or

- an examination of prospective financial information; or

- Prepare an original or amended tax return or claim for a tax refund for a contingent fee for any client.

The prohibition in (1) above applies during the period in which the member or the member’s firm is engaged to perform any of the services listed above and the period covered by any historical financial statements involved in any such listed services.

Except as stated in the next sentence, a contingent fee is a fee established for the performance of any service under an arrangement in which no fee will be charged unless a specified finding or result is attained or in which the amount of the fee is otherwise dependent upon the finding or result of such service.

Solely for purposes of this rule, fees are not regarded as being contingent if fixed by courts or other public authorities or, in tax matters, if determined based on the results of judicial proceedings or the findings of governmental agencies.

A member’s fees may vary depending, for example, on the complexity of services rendered.

Rule 501 – Acts Discreditable

A member shall not commit an act discreditable to the profession.

Under Rule 501, acts discreditable are actions by a member that may damage or otherwise impinge on the reputation and integrity of the profession. The following “acts are designated as discreditable:

- Retention of client records and auditor working papers, such as adjusting entries, necessary to complete the client’s records;

- Discrimination in employment;

- Failure follows standards and other procedures or other requirements in governmental audits; and

- Negligence in the preparation of financial statements.

A member committing a discreditable act is usually suspended or expelled from the AICPA.

Rule 502 – Advertising and Other Forms of Solicitation

A member in public practice shall not seek to obtain clients by advertising or other forms of solicitation in a false, misleading, or deceptive manner.

Solicitation by coercion, over-reaching, or harassing conduct is prohibited.

Advertising or other false, misleading, or deceptive forms of solicitation are not in the public interest and are prohibited. Such activities include those that;

- Create false or unjustified expectations of favorable results.

- Imply the ability to influence any court, tribunal, regulatory agency, or similar body or official.

- Contain a representation that specific professional services in current or future periods will be performed for a stated fee, estimated fee, or fee range when it was likely that such fees would be substantially increased at the time of the representation. The prospective client was not advised of that likelihood.

- Contain any other representations that would likely cause a reasonable person to misunderstand or be deceived.

Rule 503 – Commission and Referral Fees

- Prohibited commissions

A member in public practice shall not for a commission recommend or refer to a client any product or service, or for a commission recommend or refer any product or service to be supplied by a client, or receive a commission when the member or the member’s firm also performs for that client:

- an audit or review of a financial statement; or

- a compilation of a financial statement when the member expects, or reasonably might expect, that a third party will use the financial statement and the member’s compilation report does not disclose a lack of independence; or

- an examination of prospective financial information.

This prohibition applies during the period in which the member is engaged to perform any of the services listed above and the period covered by any historical financial statements involved in such listed services.

- Disclosure of permitted commissions

A member in public practice who is not prohibited by this rule from performing services for or receiving a commission and who is paid or expects to be paid a commission shall disclose that fact to any person or entity to whom the member recommends or refers a product or service to which the commission relates.

- Referral fees

Any member who accepts a referral fee for recommending or referring a CPA service to any person or entity or who pays a referral fee to obtain a client shall- disclose such acceptance or payment to the client.

Rule 505 – Form of Organization and Name

A member may practice public accounting only in the form of the organization permitted by law or regulation whose characteristics conform to council resolutions.

A member shall not practice public accounting under a misleading firm name. Names of one or more past owners may be included in the firm name of a successor organization.

A firm may not designate itself as a “Member of the American Institute of Certified Public Accountants” unless all its CPA owners are members of the Institute.

Comparing the Codes of Ethics: AICPA and IFAC

Although auditors must comply with the specific standards adopted in each jurisdiction, familiarity with IFAC’s International Ethics Standards Board for Accountants (IESBA) Code of Ethics for Professional Accountants (IESBA Code) in addition to the AICPA Code of Professional Conduct (AICPA Code) is a critical first step.

When specifications differ, members should comply with the more restrictive applicable standards.

More similar than different

The IESBA and AICPA codes are more similar than different, although some differences are significant.

For example, the IESBA Code is divided into three parts;

- Part A applies to all professional accountants.

- Part B, only to persons in public accounting; and

- Part C, to persons in business, is everyone who is not in public practice.

The AICPA does not apportion its principles and rules in this manner. Other differences are more substantive.

As for similarities, both codes address independence, due care, confidentiality, and the truthful reporting of information.

The principles underlying each code are similar, except that the IESBA addresses confidentiality and marketing as principles (the latter under professional behavior) applicable to all professionals.

In contrast, the AICPA Code includes these rules applicable to public practice members.

IESBA ethics requirements for professional accountants in business, such as corporate accountants, are much like those found in the AICPA Code.

However, certain IESBA guidance is more comprehensive (for example, inducements, acting with sufficient expertise).

Principles vs. rules

The IESBA Code is often called a principles-based code, while many consider the AICPA Code to be more rules-based. Similar to comparisons between IFRS and U.S. GAAP, these descriptions can be misleading.

Professional accountants must comply with the fundamental principles of the IESBA Code and apply a “conceptual framework approach” to determine their compliance with the fundamental principles whenever they know (or should know) that circumstances or relationships may compromise their compliance.

While the onus is on the professional accountant to do this, the bulk of the IESBA Code describes how the conceptual framework applies in specific situations.

Conclusion

Professional ethics refers to the accepted standards of behavior, values, and guiding principles that professionals must adhere to.

It is important to ensure that the public interest is protected and the credibility, professionalism, and quality of service of the profession are maintained. Professional organizations establish codes of ethics to guide their members in performing their job functions ethically.

Accountants have a crucial role to play in building economic well-being and must act in the public interest to maintain the reputation of their profession. Compliance with ethical guidelines helps build trust and confidence among clients and society.